Cash flow challenges don’t discriminate. Even well-established companies with strong revenue can find themselves in a pinch when liquidity is tight. Traditional banks often walk away when covenants are stretched, credit scores slip, or growth stresses collateral coverage.

That’s where Asset-Based Lending (ABL) comes in as a flexible solution designed for companies that need to put their assets to work to fuel growth.

What Is Asset-Based Lending?

Asset-Based Lending allows businesses to borrow against the value of accounts receivable, inventory, and equipment. Instead of being limited by credit score alone, ABL taps into the strength of your balance sheet.

At TAB Bank, our ABL solutions include:

- Facility Sizes: $1MM – $15MM, expandable to $25MM

- Advance Rates: Up to 85% on receivables, 50% of inventory cost (or up to 85% of NOLV with appraisal)

- Industries Served: Manufacturing, transportation, distribution, wholesale, eCommerce, pharmaceuticals, energy services, and more.

The result: liquidity when you need it most without waiting for traditional lenders to catch up.

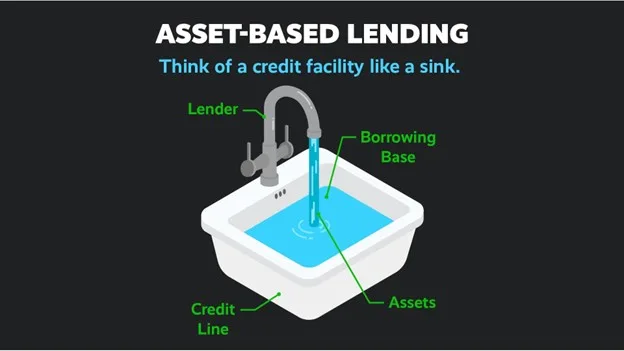

How ABL Works: The Borrowing Base

Think of ABL like a sink:

- The Credit Facility (the sink itself): The maximum size of the loan.

- The Borrowing Base (the water inside): The eligible collateral you’ve contributed.

- Available Funds (the faucet): The portion of the borrowing base you can draw upon.

Every week, borrowers submit a Borrowing Base Certificate (BBC) with supporting reports (AR aging, inventory valuations, sales reports). This ensures real-time alignment between asset value and loan availability.

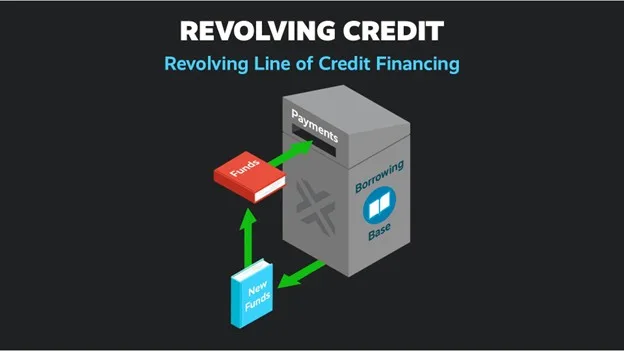

How ABL Works: Revolving Line of Credit

ABL typically operates as a revolving line of credit. This means funds can be drawn, repaid, and drawn again, just like a credit card.

This revolving structure provides flexibility, allowing businesses to smooth out cash flow cycles without needing to renegotiate terms.

A revolving line of credit is like borrowing books from the library. You take out what you need, but you must return it before you can borrow more.

This allows the client to maintain their credit facility after paying back the funds used.

Why Businesses Choose ABL

ABL is built for companies that carry assets and need flexibility in working capital. Common use cases include:

- Manufacturers funding large orders or managing seasonality

- Transportation & Logistics firms are keeping receivables and fleets moving.

- Wholesale & Distribution companies financing large inventory positions

- Energy & Pharma businesses navigating cash-heavy growth cycles

- eCommerce companies are unlocking liquidity to reinvest in marketing and stock

Recent examples from TAB Bank include:

- A $5MM facility for an Ohio manufacturer of plumbing fixture displays

- A $3.8MM facility for a Michigan transportation company needing a lender with industry expertise

- A $1.5MM facility for a California drayage company scaling pipeline growth

As Marc Karyo, CFO of CNC Precision, shared:

“I’ve closed similar loans in the past, but my TAB Bank experience has been, by far, the best… This is the banking team we’ve been looking for.”

The TAB Bank Difference

Every ABL client at TAB Bank is paired with a dedicated Relationship Manager. Their role goes beyond funding to include:

- Proactive insight into account trends

- Guidance on complementary banking solutions

- Long-term relationship building

At TAB Bank, we don’t just lend against assets. We invest in potential.

Ready to Put Your Assets to Work?

Asset-Based Lending isn’t about borrowing more; it’s about borrowing smarter. By leveraging your receivables, inventory, and equipment, you can unlock liquidity, protect operations, and invest in growth even when traditional banks say no.