Most businesses reach a point where they need some outside funding to address a wide range of issues, from seasonal peaks and valleys in revenue to securing the equipment needed to complete a potentially lucrative project. How your company accesses this financing, the approval process tied to securing it, and the ability—or lack thereof—to receive additional money are all important considerations. Companies that carefully deliberate and identify a funding option that makes sense for their needs position themselves for success.

At TAB Bank, we believe that business receivables factoring is a uniquely effective choice for business financing, offering a combination of benefits that help companies across the modern economy secure the money needed to realize their goals. Let’s look at what business receivables factoring is and what sets it apart from other financing options.

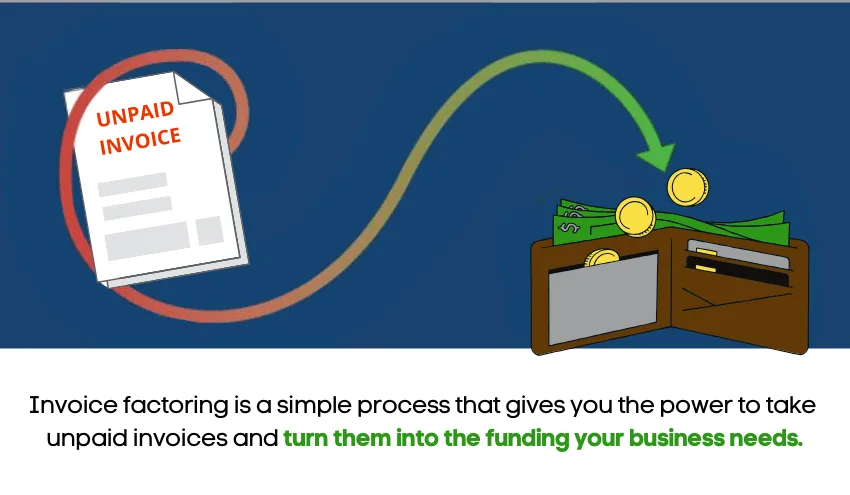

What is business receivables factoring?

Business receivables factoring, also known as invoice factoring or accounts receivable factoring, is a simple process that gives you the power to take unpaid invoices and turn them into the funding your business needs. Specifically, using invoices for products and services already provided as collateral for a line of credit that your financial institution extends to you. You don’t have to worry about using mission-critical assets like equipment, real estate, or inventory as tools to secure your financing. Instead, you use one specific resource that, for many businesses, is consistently replenished as time goes on. Additionally, your company can increase its line of credit by using additional invoices to increase the amount of credit available.

This combination of limited, clearly defined scope for the collateral tied to the line of credit and the ability to increase it as you deem necessary is powerful, to say the least. If your company requires a short-term infusion of cash due to an unpredictable emergency or wants continuing access to a line of credit for years to come, business receivables factoring can capably address that need.

What makes business receivables factoring an effective choice for business financing?

The flexibility in this type of financing is a clear advantage, allowing businesses to develop a line of credit that suits their individual needs. Instead of being locked into a specific amount, as is common with a loan, or facing the credit limits that come along with many business credit cards, your company has far more control over the process.

The speed with which you can secure financing is another important consideration. Strong owners and leaders regularly plan ahead and develop contingencies for dealing with emergencies. But even then, some issues are truly unpredictable. From a rare natural disaster to a twist of fate that leaves a company especially vulnerable or primed for a major opportunity, there are many instances where companies need money quickly.

Can my business qualify for business receivables factoring?

TAB Bank offers an online application process that can be completed in minutes, with expedited funding possible under certain conditions, including credit approval. When time-sensitive needs strike, business receivables factoring can prove to be a fast and efficient response for quickly accessing the funds you need.

Two types of business receivables factoring

There are traditionally two types of business receivables factoring: recourse and non-recourse. The main difference between the two lies in what happens if your clients do not pay their invoices. With recourse factoring, your company is responsible for all invoices, whether or not your customers pay them. If a client defaults, your business will be responsible to repay the money to the factor. With non-recourse factoring, the factoring company takes responsibility for any situations where a customer does not pay their invoice. Non-recourse factoring usually requires a high level of trust with customers and may require a larger discount rate.

Pros and cons of business receivables factoring

As with any financing option, there are pros and cons that need to be considered. Each business varies and taking your business’s specific needs into account is crucial for determining if this type of factoring is right for you. Things such as liquidity, number of customers, and relationships with clients are all things you should take into consideration when deciding whether to utilize business receivables factoring.

Pros

- Your business gets cash quick: Especially in the case of unexpected emergencies, fast cash can be a necessity

- Any size business can utilize factoring: Whether you run a small start-up or a larger company, you can benefit from the rewards of business receivables factoring

- Flexibility with your line of credit: You can often adjust your line as needed throughout your factoring contract

- Your invoices act as your collateral: There is no need to put high-risk assets as collateral, invoices act as a much lower-risk replacement

- Business can qualify even with poor or no credit: Because factoring uses outstanding invoices and accounts receivables as collateral, whether or not your business qualifies is determined more by the creditworthiness of your clients than your own company’s credit profile

Cons

- More expensive than traditional financing: Fast cash is more expensive cash, this type of financing does come with higher costs than traditional business lines of credit but can still be beneficial depending on your business

- Customers are aware that you are using invoices for factoring: Financing companies can contact your customers, and depending on your client-company relationship this could be a downside to business receivables factoring for your company

- Customers that are slow to pay can affect your available credit: If customers are not paying their invoices in a timely manner, it can have an effect on the amount that you are able to leverage

Receivables Factoring with TAB Bank

As part of our effort to build strong relationships with all of our partners, we include a dedicated relationship manager in all factoring agreements. Your relationship manager will help your company navigate the process of securing financing, as well as address your unique banking and financial needs. With this assistance, your company can make the most informed choices possible in terms of business receivables factoring, as well as learn about other potentially beneficial banking and financing options. To learn more about what TAB Bank can do for your business, get in touch with us today!

If you are looking to apply for business receivables factoring, click the link below to be taken to our online application.